.png)

What is Credit History and How to Improve Your Credit Score in the U.S.?

- Annabelle Torres

- Jan 14, 2025

- 3 min read

In the United States, to take advantage of lower mortgage rates or gain access to credit for buying a car or a home, it is necessary to have a good credit score. But what is credit history and how is a solid one built?

What is Credit History and Credit Score? And How to Improve Your Credit Score

According to Bruce McClary, Vice President of Communications at the National Foundation for Credit Counseling, "A credit score is an indicator of your overall credit health, based on how you manage your debt." In short, it tells lenders whether it's risky or not to lend you money.

Lenders use a credit score, a three-digit number, to determine whether they will lend you money and under what conditions. The higher your score, the more likely you are to get a lower interest rate, which could save you thousands of dollars in interest over time.

How Your Credit Score is Calculated

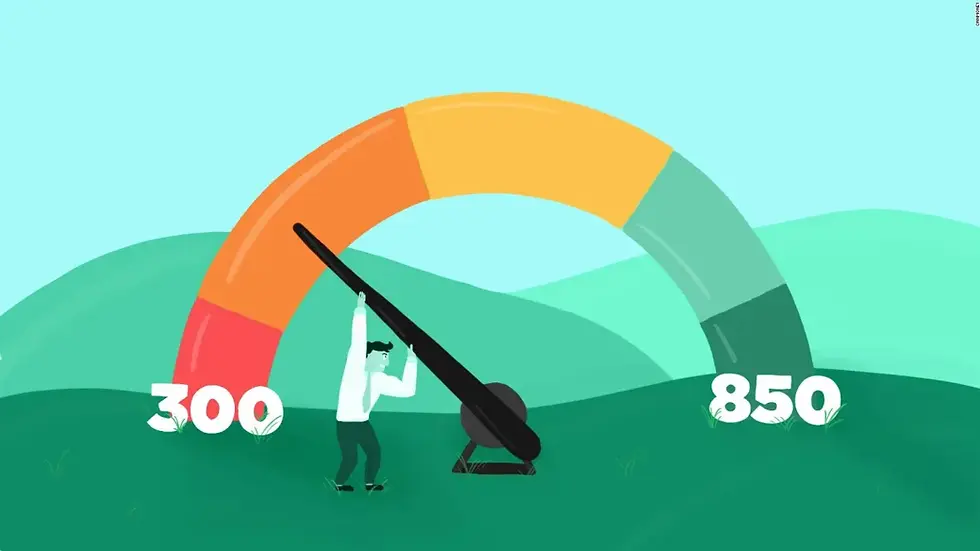

Credit agencies collect information such as your Social Security number, birth date, assets, debts, and payment history. This data is condensed into a figure between 300 and 850, which estimates the risk of lending you money. A higher score reflects lower risk.

The Importance of Checking Your Credit History

It is crucial to know your score and regularly check your credit history. Credit reports show your credit behavior, and you can check your report for free once a year from each of the three major credit agencies: Equifax, Experian, and TransUnion via AnnualCreditReport.com.

Reviewing your reports allows you to spot errors or potential fraud. Matt Schulz, a credit analyst at LendingTree, advises that one of the best ways to improve your score is to correct any errors you find in your report.

What Factors Affect Your Credit Score?

Your credit score is composed of five key factors:

Payment History (the most important factor)

Amount of Outstanding Debt (your credit utilization)

Length of Credit History

Variety of Credit Types

New Credit Accounts

Although reports do not include your score, many credit card issuers provide it for free, allowing you to monitor your credit health.

How to Improve Your Credit Score

Pay on Time: Consistently making timely payments is crucial. Late payments significantly affect your score, so it is important to catch up on any outstanding debt.

Reduce Credit Usage: Keeping your credit utilization rate below 30% is important. Paying off debts and maintaining low balances can quickly improve your score.

Do Not Close Credit Cards: Even if you've paid off your debt, closing a credit card can increase your credit utilization ratio, which may negatively affect your score.

Establish New Credit: If you're new to credit, consider opening a secured credit card or becoming an authorized user on someone’s account with a good credit history.

Keep in Mind That There’s More Than One Credit Score

FICO is the most widely used system, but there are other variants like VantageScore that many lenders also use. Although scores may vary slightly between systems, they generally move in the same direction. If one of them drops significantly, it could indicate an error or problem in your report.

Conclusion

A good credit score is essential for obtaining better loan, mortgage, and even insurance terms. Improving it takes time and effort, but with responsible habits and consistent monitoring, you can make significant progress that will benefit your finances in the long run.

Comments